- The import quotas for Q4 2025 on hot-rolled coil (HRC) and cold-rolled coil (CRC) from Turkey and Taiwan to the EU have already been fully used.

- The upcoming CBAM, anti-dumping (AD) duties, and newly proposed import quotas are prompting buyers in the EU market to accelerate imports ahead of schedule.

- Meanwhile, European mills have raised their offers for HRC, CRC, and hot-dip galvanized (HDG) steel.

- The long steel market remains more stable, though import volumes are high.

Quarterly Tariff Rate Quotas (TRQ) Nearly Exhausted

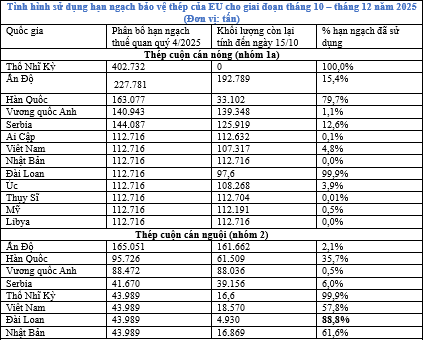

The quarterly tariff rate quotas for some steel products covering the period from October to December 2025 have been almost fully used, reflecting stronger demand amid shifting EU trade policies and expectations of tighter market conditions in the near future.

Hot-Rolled Coil (HRC)

For hot-rolled coil, Turkey and Taiwan have already exhausted their entire Q4 2025 quota allocations, while South Korea’s quota was nearly full as of October 15, 2025, according to European Commission customs data.

European importers have been rushing to book HRC cargoes for Q4 2025 delivery in order to receive shipments before 2026—when the EU’s Carbon Border Adjustment Mechanism (CBAM) takes effect and imported goods will be subject to carbon levies.

In contrast, quota utilization by traditional suppliers such as Egypt, Vietnam, and Japan remains very low (see table below), as all three countries are currently subject to EU anti-dumping duties (AD).

In addition to CBAM and AD duties, the European Commission on October 7 announced a sweeping proposal to reform safeguard measures on steel imports. The plan includes cutting duty-free quotas by about 47% and imposing a 50% tariff on import volumes exceeding the new thresholds.

Most market participants expect the new framework to replace the current safeguard system once it expires on June 30, 2026. However, some believe the Commission may introduce it earlier, as soon as April 1, 2026.

The uncertainty surrounding these changes and the anticipated disruption of steel imports into Europe in Q1 2026 have prompted European steelmakers to raise HRC prices for December 2025–January 2026 delivery.

On October 13, leading European producer ArcelorMittal announced offer prices of €630/tonne (≈US$730) for December 2025 and €650/tonne for January 2026, depending on the region.

From October 21–24, the 17th Blechexpo Trade Fair will take place at Messe Stuttgart, Germany. (The exhibition showcases the entire sheet metal processing chain, from cold forming to cutting, joining, and related thermal and mechanical processes.)

Several market participants anticipate further price hikes for flat steel products during the event.

Cold-Rolled Coil (CRC) and Hot-Dip Galvanized (HDG) Steel

The situation is even tighter in downstream flat steel markets, especially for cold-rolled coil.

As of October 15, 2025, Turkey and Taiwan had nearly used up their Q4 quotas, while Japan and Vietnam had already consumed more than half.

Furthermore, on September 18, the European Commission launched an anti-dumping investigation targeting CRC imports — affecting more than half of the EU’s total CRC import volume.

With the AD probe, the upcoming CBAM, and stricter import quotas under the proposed trade framework, the European CRC market is expected to face major volatility in 2026.

Imported CRC continues to dominate the European market, as EU mills rarely sell CRC externally; most of their CRC output is used internally for producing HDG — a product with higher profit margins.

Thus, tighter trade restrictions on imported CRC could make it increasingly difficult for European steel service centers to secure material supplies.

ArcelorMittal is now targeting €730/tonne ex-works for CRC deliveries in December 2025 and €750/tonne for January 2026.

Currently, most EU mills have no CRC availability left for 2025, and many have already sold out into 2026.

As a result, most market participants expect domestic CRC prices in Europe to rise during Q4 2025 and Q1 2026 as import supply tightens.

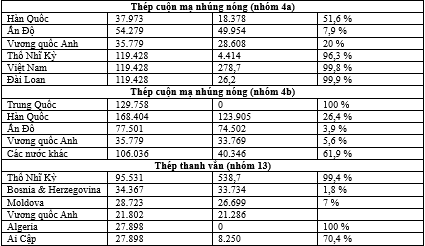

For HDG, quota usage has also been strong as buyers rush to place orders before CBAM enforcement.

European mills have raised HDG offer prices for December 2025–January 2026 delivery to €730–750/tonne across Northern and Southern Europe.

Long Steel

Unlike the flat steel market, news of new import restrictions and the introduction of CBAM has so far caused little price volatility in the long steel sector across most parts of Europe.

As of October 15, 2025, according to European Commission customs data, Turkey and Algeria had already exhausted their quotas for rebar, while Egypt had used over 70% of its Q4 2025 quota.

In addition, Ukraine has been supplying large volumes of long steel to the European market this year.

In the first seven months of 2025, Ukraine exported 140,978 tonnes of rebar to the EU — compared with just 29,842 tonnes during the same period in 2024.

Ukrainian suppliers currently enjoy exemption from quotas and out-of-quota duties under the EU’s safeguard framework, as the European Commission has extended the suspension of safeguard measures on Ukrainian steel for another three years, starting June 6, 2025.

Hoàng Trung